Disclaimer: This Blog,its owner,creator & contributor is neither a Research Analyst nor an Investment Advisor and expressing opinion only as an Investor in Indian equities. He/She is not responsible for any loss arising out of any information, post or opinion appearing on this blog.Investors are advised to do own due diligence and/or consult financial consultant before acting on any such information. Author of this blog not providing any paid service and not sending bulk mails/SMS to anyone.

The RBL Bank–Emirates NBD deal is not just about one bank being acquired by another. It is a story of

choice, correction, and capital finding direction.

And before we decide whether this is an opportunity or a trap, we must slow down and understand the psychology behind it.

A Simple Question First

Why would a profitable, well-established Middle Eastern bank commit nearly ₹27,000 crore into a mid-sized

RBL Bank has clearly struggled in recent years?

Because smart capital doesn’t chase headlines. It chases future probability curves.

Emirates NBD is not betting on what RBL is today. It is positioning itself for what RBL could become if discipline meets structure.That distinction matters.

The RBL Reality: Not Broken, But Bruised

RBL is not a weak bank. But it is a tired one.

A bank that expanded fast, paid a price for aggressive lending, faced regulatory intervention and then

chose the harder path: repair instead of denial.

Financially, RBL today suggests: – Improving asset quality – Stabilising profitability – But limited growth capability due to capital constraints.

It is like a patient who is stable, but still not strong enough to run. It requires nourishment, discipline and time.

And this is where Emirates NBD enters — not as a saviour, but as a strategic partner with patience.

What This Deal Actually Signals

Markets often misunderstand deals like this. They ask: “Is this bullish or bearish?”

A better question is: “Does this improve the quality of the business long-term?”

Here’s what changes structurally: – Capital adequacy strengthens – Governance improves – Risk discipline

gets institutional backing – Operational efficiency becomes a focus

But no deal magically converts average management into exceptional execution overnight.

Time is still the most important variable.

The short-term thinker sees a spike and asks: Should I buy now? The long-term thinker asks: Will this bank be meaningfully stronger in 3 years?

The decisive factor is not the acquisition. It is how RBL behaves after the deal completes.

Monitor things that matter, not things that excite: – Cost-to-income ratio improvement – Loan book quality -ROA and ROE trend consistency – Stability of leadership – Cultural integration

These will determine whether this is a turnaround or a temporary re-rating story.

A Broader Pattern Emerging

This deal is part of something larger.

Global capital is not speculative about India. It is becoming deliberate.

Foreign institutions are buying platforms, not trading stocks. They are choosing systemic exposure to India’s credit cycle.

So, What Should a Sensible Investor Do?

There is nothing glamorous about patience. Yet it is the rarest skill.

If you’re considering RBL today, the mindset should be this:

Not — Will this double in six months?

But — Is the probability of long-term improvement increasing?

If the answer is yes, then slow accumulation with discipline and observation may make sense. If not, then it remains just another story in a noisy market.

Final Reflection

The RBL–Emirates deal is not a celebration point. It is a transition point.

And transitions are best judged not by announcements, but by habits that follow.

In the end, money always finds efficiency. And businesses that respect capital eventually earn capital.

The story of RBL will now unfold in silence — in numbers, governance, and execution.

That quiet journey will decide whether this deal becomes a case study of transformation… Or just another chapter of market optimism.

Written in the spirit of clarity, patience and long-term thinking.

This document explores the characteristics of early-stage multi-bagger stocks, focusing on identifying businesses that whisper potential through financial metrics, promoter actions, and strategic pivots. It outlines ten key principles to guide investors in uncovering undervalued opportunities before they become mainstream.

1️⃣ Turnarounds look ugly — until they don’t

The most significant investment returns often come from companies that have overcome past challenges. Look for businesses that are:

Exiting broken verticals: Divesting from unprofitable or underperforming segments.

Showing fresh promoter intent: New leadership or a renewed commitment from existing management.

Experiencing working capital revival: Improved cash flow and efficient management of current assets and liabilities.

The key is to identify when the negative noise surrounding the company subsides, signaling a potential re-rating.

2️⃣ Low P/E + High EPS Momentum = Valuation Arbitrage

A powerful combination for identifying undervalued stocks is:

Single-digit P/E: A low price-to-earnings ratio suggests the stock is cheap relative to its earnings.

Double-digit EPS: Strong earnings per share growth indicates a healthy and expanding business.

Improving trend: Consistent positive momentum in both P/E and EPS.

This scenario often represents a coiled spring, ready for a significant upward revaluation as the market recognizes the company’s true potential.

3️⃣ Brands multiply margins

When a company transitions from selling commodities to building a consumer brand (B2C), it can dramatically increase its profit margins. This is because:

You’re selling a perception: Branding creates perceived value, allowing for premium pricing.

4️⃣ Export Niche ≠ Noise

Small Indian companies that quietly dominate global niche markets can be highly profitable investments. These businesses often exhibit:

Fat RoCE: High return on capital employed, indicating efficient use of resources.

Low competition: A specialized market with limited players.

Repeat international orders: Consistent demand from overseas customers.

These companies may not be in the headlines, but their financial performance speaks volumes.

5️⃣ Unregulated niches inside regulated industries are gold

Look for opportunities within regulated sectors where certain segments operate without price controls or strict oversight. For example:

Fertilizers = controlled. Micronutrients = not.

Power = regulated. Gearboxes = not.

The key is to find pockets where:

Pricing is free: The company can set its own prices based on market demand.

Demand is sticky: Customers are reliant on the product or service.

6️⃣ Promoter actions > Analyst coverage

Pay more attention to the actions of company insiders than to analyst reports. Specifically:

Open-market purchases by insiders: When promoters buy shares in the open market, it signals strong confidence in the company’s future prospects.

Insider buying is a more reliable indicator than broker notes or media hype.

7️⃣ Over-advertised = Under-delivered

Be wary of companies that engage in excessive public relations and marketing, especially if they also exhibit:

No dividends: Failure to share profits with shareholders.

Mystery projects that never complete: Unclear or delayed initiatives.

These are often signs of a company that is more focused on appearances than substance.

8️⃣ “Tech-flavored” companies with no real product = Avoid

Avoid companies that heavily promote their use of technology but lack a solid business foundation. Look out for:

Buzzword overdose: Excessive use of trendy tech terms without clear application.

No unit economics: Inability to demonstrate profitability on a per-unit basis.

No customer clarity: Lack of a well-defined target market or customer base.

Prioritize transparency and tangible results over hype and empty promises.

9️⃣ “Dirty” businesses with ESG tailwinds will shine

Consider investing in companies involved in industries that are currently perceived as environmentally unfriendly but are poised to benefit from the growing focus on sustainability. Examples include:

Recycling

E-waste management

Sustainable materials

These businesses may not be popular today, but they have the potential for significant growth as ESG (environmental, social, and governance) factors become more important to investors.

🔟 Be a realist

When evaluating potential investments, focus on the fundamentals:

Real problem: The company solves a genuine need or pain point.

Growing profits: The company is consistently increasing its earnings.

Honest promoters: The company is led by ethical and trustworthy management.

Final Thought

The best investments are often those that are overlooked or misunderstood by the market. To find early-stage multi-baggers:

Find them: Seek out companies that meet the criteria outlined above.

Study them: Conduct thorough research to understand their business model, competitive landscape, and growth potential.

Hold them: Be patient and allow the company time to execute its strategy and realize its full potential.

In today’s world, we often rank people by the size of their bank accounts, companies, or public reach. Subconsciously, we treat wealth as the highest form of intelligence or success — as if net worth equals self-worth.

But numbers don’t tell the whole story.

Money can measure scale, but not soul. You can be rich in wealth and poor in peace. You can lead empires and still feel empty inside. What truly matters — wisdom, kindness, courage, inner stillness — can’t be captured on a balance sheet.

We live in a society obsessed with external metrics. But real value often lies in the unseen: character, clarity, and how deeply one lives their truth.

Those who can look beyond financial rankings — and see the whole human — are the ones who truly understand wealth.

BRAINBEES (FIRST CRY): The Board approved an incremental investment in Globalbees Brands Private Limited, a subsidiary, by subscribing to Compulsory Convertible Preference Shares. The approved amount is Rs. 1,46,00,94,000, slightly higher than the initially approved Rs. 1,46,00,00,000. This investment is part of a Series C2 Share Subscription Agreement and will be made in one or more tranches.

Additional investments were approved in Firstcry Management DWC LLC, a wholly owned subsidiary, amounting to AED 32 million. This capital will be further invested in Firstcry Trading Company in Saudi Arabia (up to SAR 28 million) and Firstcry Retail DWC LLC in the UAE to support business expansion efforts.

INLFECTION POINT:

Particularly the substantial investment in its subsidiary Globalbees Brands Private Limited and the expansion funding for its Middle East operations. These moves suggest a shift from consolidation to aggressive growth and international expansion.

Middle East Expansion: Brainbees has made strategic investments in the Middle East (UAE and Saudi Arabia) through subsidiaries like Firstcry Management DWC LLC and Firstcry Trading Company. This region is a key growth focus for GlobalBees to scale its brand portfolio internationally.

REASON FOR THIS INVESTMENT :

Globalbees, the company’s brand aggregation and incubation arm, saw a 30% YoY increase in revenue and an 856% surge in adjusted EBITDA, turning positive at INR 22 crores. This demonstrates successful scaling and operational leverage in the newer business vertical

KEY NOTABLE POINTS :

PAT and free cash flow positive in FY25

Higher margin, improved retention, and gross margin expansion

856% YoY EBITDA growth, INR 22 crore positive

New growth vectors and market diversification

78% of FirstCry’s GMV (GROSS MECHANDISE VOLUME )comes from online and 22% from offline stores. Importantly, 38% of GMV in top cities comes from customers who shop both online and offline, showing strong omni-channel (STORNG ONLINE AND OFFLINE SALES POINT) engagement.

Suumaya Industries Ltd exhibits multiple red flags indicative of financial misconduct, fund diversion, and governance breakdown over the many years. Key concerns include aggressive capital raising through rights and preferential issues with unclear or inconsistent fund deployment, significant anomalies in financial statements such as sharp divergences between CFO and PAT, surges in receivables and payables, and heavy related party transactions.

Suumaya Industries has raised funds through multiple routes, including rights issues and a large preferential issue in August 2023.

Suumaya Industries Ltd has repeatedly used equity-based fund-raising mechanisms—preferential allotments, warrant conversions, and public/bonus issues—over the past several years. This pattern, when cross-referenced with financial anomalies and related party dealings, strongly suggests a risk of fund diversion through these routes.

Frequent Preferential Allotments and Warrant Conversions: The company has raised capital via preferential issues and warrant conversions almost every year since lsiting, often at significant premiums. This aggressive capital raising, especially through private placements and preferential routes, is a classic setup for fund diversion—funds are raised ostensibly for business growth but may be routed elsewhere through opaque channels.

For instance, despite significant capital raising, capital expenditure (capex) and fixed assets have remained largely stagnant or inconsistent .

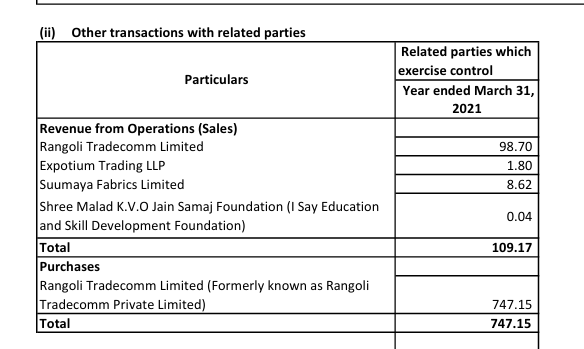

Related party transactions are substantial, with purchases from Rangoli Tradecomm Limited exceeding Rs 747 Cr and significant trade payables to the same entity (Rs 715.65 Cr in FY21), indicating possible circular transactions or fund routing

Financials: Patterns, Anomalies & Fabrications:

Sharp divergence between Cash Flow from Operations (CFO) and Profit After Tax (PAT), with PAT rising sharply in recent years

first company has surged payable through related party transactions to inflate sales and piled up inventory then followed by Surges in trade receivables.

It looks really good to see growth of the topline, but as a prudent investor one has to dig further when you see sudden surge in growth

OPERATING PROFIT AND PAT JUST AN accounting entry in books real cash realisation we will see in your SINDOOK or Cash flow .

गल्ले में पैसे होने चाहिए” only books main Nahi.

Here as an investor if anyone paid attention in cash flow would have identified easily what exactly company has done.

lets not complicate further and look at few odd figures which one can identify just going through a financial statement.

SURGRS IN SALES = ATTRACTIVE FINANCIAL NUMBERS TO TRAP RETAIL INVESTOR WHO DOESNT LOOK BEYOOND SALES AND PROFIT.

HOW THEY COOKED AND FOOLED MANY :

I WILL NOT TALK EXACT NUMBERS RATHER WILL LOOK INTO THE GROSS PICUTRE..

IN 2020,THE COMPANY WAS QUOTING RS 100 CR MARKET CAP ,GONE UP TO 20X ++ SAY 2200 CR Market cap

NOW QUOTING AT 19 CR ,WIPED OUT 2180 CR. SUCH AN EASY WAY TO MAKE MONEY AND TRAP RETAIL BY ANNOUCING ONE IPO.

HENCE ALWAYS AVOID BUSINESSES WITH SURGE IN SALES BUT CASH FLOW IS NOT IN SYNC WITH PROFIT .

The company reported extremely high sales figures that were not backed by actual cash flows. For example, However, during this period, the company’s cash flows from operations were a very small percentage of the recorded revenue.

In FY21 and FY22, cash flow from operating activities constituted only 0.39 per cent and 0.10 per cent, respectively.

During this period, the company’s shares experienced an exceptional surge from Rs 62.25 apiece in October 2020 to a peak of Rs 701.8 in July 2021.

The company engaged in circular trading, where transactions were repeatedly recorded among related entities to artificially boost turnover and valuations. Only about 10% of the transactions were legitimate, while the rest were fabricated to mislead investors and inflate share prices. Promoters diverted funds for personal gain and used complex transactions to “clean up” their books.

The promoters, including key executives like Ushik Gala and Ishita Gala, were barred by SEBI from holding any directorial or key positions due to their involvement.

During the COVID-19 pandemic, Suumaya Industries claimed to supply agro products under the Haryana government’s “Need to Feed” program, but investigations found no evidence of any contract or actual supply. Fake lorry receipts and invoices were created to substantiate these false claims.

Promoter Playbook: Tactics, Shells, and Related Entities:

Promoter share pledging is significant, with insiders like Ushik Gala and Ishita Gala selling shares worth crores recently, indicating possible financial stress or exit attempts.

Loans to promoters and related parties, coupled with large trade transactions with entities like Rangoli Tradecomm Limited (likely promoter-affiliated), suggest circular fund flows and value extraction through backdoor ownership or shell companies.

Insider trading data shows concentrated selling by promoter individuals in June 2024, coinciding with fundraising rounds, possibly to manage liquidity or reduce exposure.

The promoter group’s strategic decisions, including board changes and auditor switches, appear timed around fundraising events and share pledge releases, indicating attempts to manage market perception and regulatory scrutiny.

Governance Failures & Regulatory Arbitrage

Frequent auditor changes and limited transparency in related party disclosures undermine governance.

Cross-Case Comparisons

Similarities with DHFL and PC Jeweller cases include aggressive fund raising followed by opaque related party transactions and promoter pledging leading to value extraction.

Like Satyam, Suumaya shows divergence in reported profits vs cash flows and sudden changes in auditor and board composition.

Systemic loopholes exploited include weak enforcement of related party transaction disclosures, promoter pledge monitoring, and delayed regulatory intervention.

Learning for an Investor from the Suumaya Industries Fraud Case

1. Beware of Aggressive Fundraising Without Clear Asset Growth

Suumaya raised large sums repeatedly via preferential allotments, warrant conversions, and rights issues, yet showed little corresponding capital expenditure or asset creation. This mismatch is a classic red flag indicating possible fund diversion or misuse rather than genuine business expansion24.

2. Scrutinize Related Party Transactions and Circular Deals

The company’s financials revealed massive related party transactions and circular trading patterns inflating turnover artificially. Such practices often mask siphoning of funds to promoter-affiliated or shell entities, undermining real value

3. Watch for Divergence Between Reported Revenues and Actual Cash Flows

Suumaya reported skyrocketing sales but received only a fraction in cash, with dues mysteriously written off. This disconnect between reported earnings and cash inflows is a strong indicator of fictitious sales and financial manipulation.

4.Investor Due Diligence Must Go Beyond Surface Financials

Relying solely on reported revenues and profits without analyzing cash flows, related party dealings, auditor reports, and promoter activities can be perilous. Investors should demand transparency and perform forensic-level scrutiny, especially in companies with complex fundraising and ownership structures.

Got it! Here’s a refreshed version of the original message with new phrasing and different examples, but the same core message and tone—perfect for sharing as a fresh post:

Smart Doesn’t Mean Successful We often assume that success—especially in investing—comes from intelligence. That if we read enough books, learn complex strategies, and talk like experts, we’ll automatically make the best decisions.

But the real world doesn’t work that way. The market doesn’t reward how smart you sound or how detailed your research is. What it really measures is your emotional discipline. Your edge isn’t your IQ—it’s your ability to stay calm, patient, and grounded when things get unpredictable.

You’ll notice this: even those with years of experience sometimes react emotionally when uncertainty strikes. They chase trends, freeze during downturns, or constantly shift strategies. On the other hand, someone with basic knowledge but steady habits often ends up ahead. Why? Because progress comes from balance and behavior, not brilliance.

Learning and thinking critically are valuable, no doubt. But don’t confuse intelligence with control. If knowledge alone were enough, classrooms would be full of future billionaires. But success in the real world comes from consistency, self-control, and the ability to stick to a plan when things get tough.

So remember: it’s not about how much you know, but how well you act when it matters. Knowing isn’t winning. Doing the right thing at the right moment is.

Privi Speciality Chemicals Ltd is India’s leading manufacturer, supplier, and exporter of aroma and fragrance chemicals. The company is globally recognized as a trusted partner and preferred supplier of bulk aroma chemicals used in soaps, detergents, shampoos, and fine fragrances.

Company Overview

Founded: 1992 by Mr. Mahesh Babani, who remains the Managing Director.

Headquarters and Facilities: State-of-the-art integrated manufacturing plants located in Mahad (Maharashtra) and Jhagadia (Gujarat), equipped to perform complex chemical reactions such as hydrogenation, condensation, Grignard reactions, pyrolysis, reactive distillation, and continuous distillation to ensure high quality and consistency.

Product Portfolio: Over 50 aroma and fragrance chemicals, including key molecules like Dihydromyrcenol (DHMOL), Amber Fleur, Terpineol-Pine Oil, Galaxmusk, Florovane, Indomerane, and Amber Xtreme. DHMOL is used in 99% of contemporary perfumes as a freshness molecule, highlighting Privi’s dominant market position.

CAPACITY EXPANSION :Plants operated at 85–90% capacity; expansion planned from 48,000 MT to 54,000 MT by March 2026

Premium Product Pipeline

They’re doubling down on high-margin aroma and fragrance chemicals like Indomerane, Florovane, and Amber Woody Xtreme. These are gaining traction in personal and home care, where demand remains resilient and pricing power is higher.

Launched new products: Indomerane, Florovane, Amber Woody Xtreme – used in personal care and home care

Improving asset turnover ratio from 1.4x to 1.7x, enhancing capital efficiency

Geographical Diversification: With only ~7% of revenues from the U.S., they’re emphasizing growth in underpenetrated and fast-developing markets like Africa, Asia, and the Middle East. They’re also leveraging “China Plus One” and “Europe Plus One” strategies as global supply chains pivot toward diversification.

Customer Count Is Expanding: Management stated they’ve moved from primarily servicing three key customers to now engaging with six top-tier clients, and are already working with most of the global top ten fragrance and FMCG players.

New Geographies, New Clients: They’ve gained at least five new sizable customers, especially from Africa, Asia, and the Middle East, aligning with their geographic diversification strategy.

Deeper Wallet Share + New Additions: While growing the number of customers, they’re also increasing share of business from existing clients through co-development and tailored solutions

Market Size and Growth Projections

The market was valued at approximately USD 5.60 billion in 2023 and is projected to grow to around USD 5.88 billion in 2024.

Asia Pacific dominates the aroma chemicals market, holding around 30-40% market share as of 2023-2025, driven by countries like China, India, and Japan.

Emerging markets in the Middle East, Africa, and Latin America are expected to contribute to future growth due to rising consumer awareness and expanding personal care industries.

Market Drivers and Trends

Increasing consumer preference for natural, organic, and sustainable aroma chemicals is a key growth driver, especially in developed economies.

The aromatherapy industry’s expansion, driven by rising demand for natural essential oils and fragrances for wellness and stress relief, is boosting aroma chemical consumption..

Growth in cosmetics, toiletries, soaps, detergents, and food & beverage sectors is fueling demand for aroma chemicals due to their role in enhancing sensory appeal.

Advances in biotechnology, green chemistry, and digital formulation tools are enabling innovation in aroma chemical production, including nature-identical and biodegradable compounds.

Regulatory scrutiny and sustainability initiatives are shaping market dynamics, with companies focusing on eco-friendly sourcing and manufacturing processes.

FINANCIAL HIGHLIGHT

ABLE TO HOLD MARKET SHARE OVER LAST MULTIPLE YEARS SHOWS THE TRUST AND ABILTY OF THE COMPANY BUILD OVER A YEARS.

INCREASING PROFIT MARGIN : NOT ONLY SCALE UP ALSO ABLE TO SUSTAIN PROFIT MARGIN SHOWS COMMAND IN GLOBAL MARKET

OCF >PAT , NUMBER OF PUBLIC SHAREHOLDERS SLOWLY DECREASING , STABLE BALANCE SHEET WITH HIGH ASSET ADDITION SHOWS PROPER USE OF RESERVE AND DEBT TOWARDS GROWTH

PROFIT AND PRICE GROWTH IN SYNC =FAIRLY VALUED .

NOT A RECOMMENDATION TO BUY OR SELL. KEEPING RECORDS AS MY FUTURE REFERENCE .

The Cost Your Don’t See We always talk about risk in investing, like market risk, interest rate risk, valuation risk, business risk, and management risk. But I think one of the biggest risks is the one we don’t think about much, or name.

It’s distraction. Just constantly being pulled in different directions, often mindlessly. One day you’re following a long-term plan, next day you’re wondering if you should be doing what everyone else is doing. Someone posts a 3x return on some random stock and suddenly you’re questioning everything. It doesn’t seem like a big deal in the moment. But over time, it adds up. You lose clarity. You lose momentum. You start drifting. This applies to life, too. The more you’re caught up in what everyone else is doing in their careers, their houses, or their vacations, the harder it becomes to hear your own voice.

The cost of all this distraction is not immediate. It shows up over time. In missed compounding. In restlessness. In feeling like you’re always moving but not really getting anywhere.

I think the best investors, and honestly, the calmest people, are just the ones who’ve figured out how to stay focused on their own path, even when it’s boring. This is because not all losses show up in your portfolio. Some show up in your peace, too. But, only if you’re looking, without any distraction.